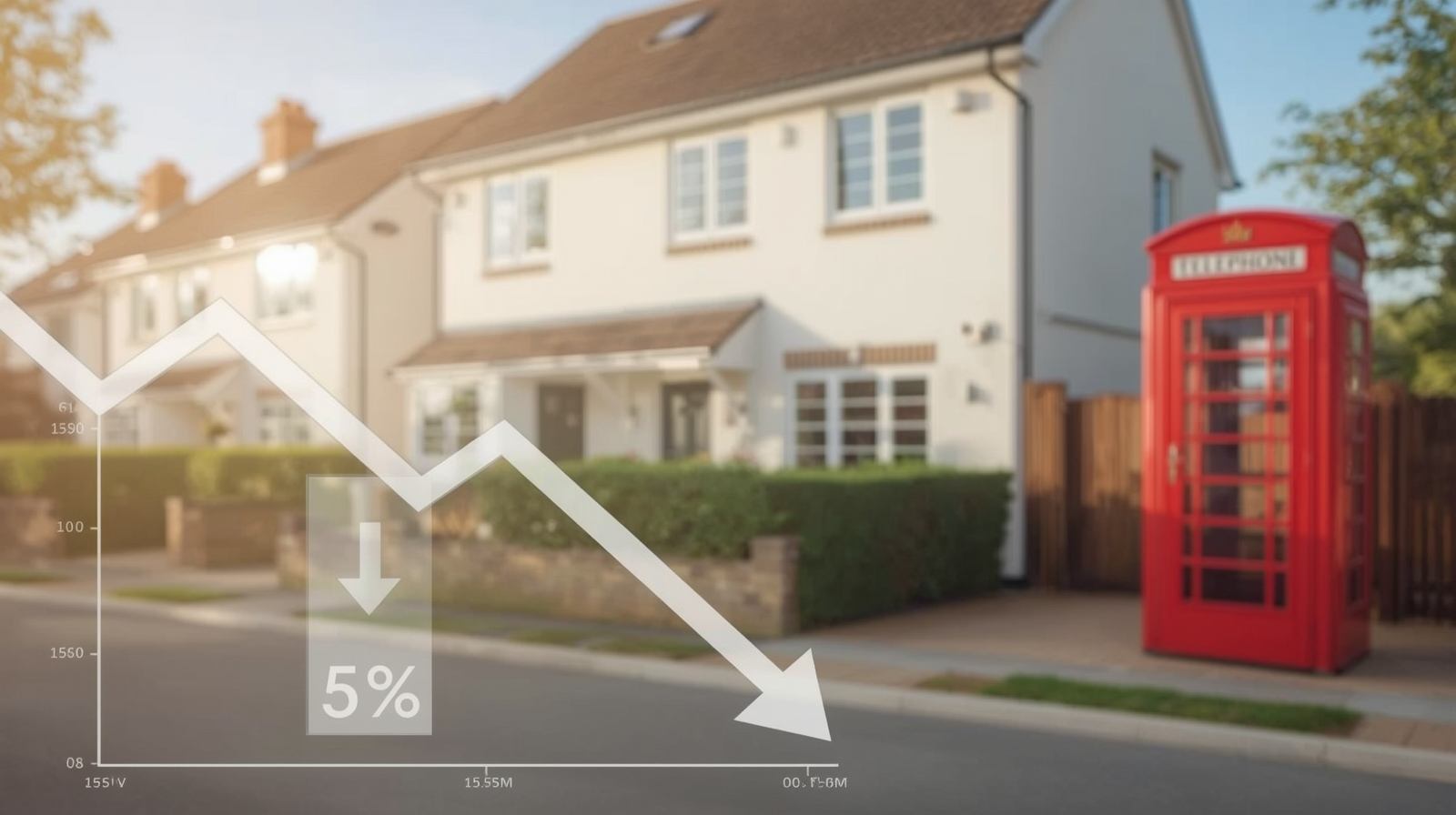

In May 2025, UK mortgage rates dropped below the symbolic 5% threshold, marking a significant milestone in the mortgage market. This decline reflects easing monetary conditions, heightened competition among lenders, and growing optimism across the housing sector.

In this article, let’s dive into the facts, figures, and implications of this shift.

Why Have UK Mortgage Rates Fallen Below 5%?

1. Bank of England Base Rate Cut

The Bank of England recently lowered the base rate from 4.50% to 4.25%, reducing the cost of lending for banks. When the base rate drops, mortgage lenders respond by lowering fixed-rate and variable-rate products.

2. Falling Swap Rates

Swap rates—which lenders use to price fixed-rate mortgages—have been falling for several weeks. Lower swap rates make it cheaper for lenders to offer competitive mortgage deals, pushing average mortgage rates down.

3. Increased Competition Among Lenders

With demand slowing in early 2025, lenders are pushing more attractive offers to bring borrowers back into the market. This has triggered a “mini price war,” where lenders reduce interest rates to win new business.

Headlines And Key Figures

Metric | May 2025 Snapshot |

Average 2-year Fixed Rate | ~4.99% |

Average 5-year Fixed Rate | ~4.99% |

Bank of England Base Rate | 4.25% (cut from 4.50%) |

Best 2-year Fixed Deals | ~3.7-3,8 for well-qualified borrowers |

Best 5-year Fixed Deals | ~3.8-3.9% for low LTV/high equity borrowers |

What this Means for Current Homeowners

1. Lower Monthly Payments

A mortgage rate below 5?n reduce monthly repayments by hundreds of pounds, especially for those switching from rates above 6% or 7% from last year's reports.

2. New Remortgaging Opportunities

Homeowners coming to the end of fixed deals now have more favourable refinancing options. Many are locking in 5-year deals around 4-5%, creating stability and reducing long-term financial pressure.

3. Better Affordability Stress Tests

With rates easing, lenders’ affordability assessments have relaxed slightly. This means some borrowers who previously failed stress tests may now qualify for new deals.

Impact on First-Time Buyers

1. Improved Affordability

Lower rates reduce monthly payments, making mortgages more manageable for first-time buyers. Although house prices remain relatively high, lower interest costs aid in bridging the affordability gap.

2. More Mortgage Products Available

As lenders compete, more products with lower deposits, flexible terms, and incentives are returning to the market. This move will prove best for all.

3. Renewed Market Confidence

A sub-5% market restores confidence and encourages more first-time buyers to begin house-hunting again. This uptick in demand is already being felt in estate agencies across the UK.

How Falling Rates Affect the Housing Market

1. Increased Buyer Activity

A drop below 5% signals stability, encouraging buyers who paused their plans last year to return. This may lead to gradual growth in property transactions over the coming months.

2. Slight Upward Pressure on Prices

While falling rates are positive, increased demand could push house prices up again. Analysts expect modest price growth during the second half of the year if rates continue to decline.

3. More Movement in the Remortgage Market

Millions of households whose fixed deals expire in 2025 are expected to remortgage now that rates are more attractive. This movement will boost lender activity and increase turnover in the mortgage sector.

Risks and Things to Consider

Even though rates have fallen, borrowers should be aware of:

1. Not Everyone Will Qualify for the Lowest Rates

The best deals (3.7–3.9%) are typically for borrowers with:

Strong credit scores

Low loan-to-value ratios

Stable income

Others may still face rates slightly above 5%.

2. Rates Could Fall Further

Economists predict more Bank of England cuts this year. Borrowers must choose between locking in now or waiting for potentially lower rates. This decision involves risk and timing, which is concluded after reports are managed and navigated properly by experts.

3. Economic Uncertainty

Inflation, wage growth, and global market changes can influence future interest rate decisions. If inflation rises again, mortgage rates may stall or increase.

4. Fixed vs Variable Considerations

Fixed-rate mortgages offer stability and are ideal when rates are unpredictable.

Variable-rate mortgages may drop further, but they carry the risk of rising again.

Borrowers must assess their risk tolerance and financial stability before choosing.

Expert Predictions for the Next 6 Months

Financial analysts expect:

Mortgage rates may fall to around 4.5% on average.

Best fixed-rate offers could reach 3.5% if swap rates continue to decline.

Housing demand will increase steadily but not dramatically.

Lenders will continue to reduce rates to attract customers.

Final Thoughts

Homeowners, purchasers, and the real estate market as a whole are greatly relieved that UK mortgage rates have dropped below 5%. After years of economic difficulties, it represents a change toward more stability. Many people are finding it simpler to plan real estate purchases or remortgage their homes due to reduced borrowing prices, heightened lender competition, and rising consumer confidence.

Even when the market is strengthening, borrowers still need to take potential rate changes, financial risks, and qualifications into account. Overall, the current trend presents a positive view for anyone entering or reentering the UK property market, albeit the upcoming months will be crucial.

Frequently Asked Questions (FAQs)

1. Why have UK mortgage rates fallen below 5%?

Mortgage rates dropped due to a lower Bank of England base rate and falling swap rates. Increased competition among lenders also helped push rates down.

2. Will mortgage rates continue to fall this year?

Experts predict gradual declines if inflation stays under control. Rates may reach around 4.5% on average by the end of the year.

3. Is now a good time to remortgage?

Yes, many homeowners can secure better deals compared to last year’s 6–7% rates. However, the choice depends on personal finances and long-term goals.